PROGETTARE IL FUTURO. IL CASO ITALIA https://www.barnesandnoble.com/w/progettare-il-futuro-ascanio-graziosi/1143656413

L’andamento dei cicli economici succedutisi nelle passate quattro decadi nell’economia internazionale ha avuto riscontro nell’economia italiana in quanto interconnessa e interdipendente con il Sistema con cui condivide i valori. Il Dr Graziosi ha affermato che la narrazione dei fatti economici se non è partigiana, è perlomeno sostenitrice del potere di volta in volta dominante. All’estero la situazione è pressocché simile, ma la narrativa è meno omologata all’Editoria di appartenenza. Dai risultati della ricerca è emerso che l’obiettivo dell’inclusione finanziaria è stato conseguito a detrimento della sostenibilità. Da questo dato di fatto, l’Autore ha proposto il Modello ECONOMIA-BASATA SULLE COMUNITÀ che nel rispetto dei principi dell’Agenda ONU 2030, ne reinterpreta l’applicazione. Il nuovo Governo sembra proporre un ritorno nostalgico a valori ancorché revisionati pur sempre obsoleti, e palesa inesperienza ministeriale associata a insufficienza comunicativa. Inoltre, mostra il perseguimento di una politica di distinguo nel contesto Europeo e non solo.

THE THEORY OF CHANGE APPLIED TO FINANCE FOR DEVELOPMENT http://reader.ilmiolibro.kataweb.it/v/1252660/the-theory-of-change-applied-to-finance-for-development_1268103

The Author elaborated the Theory of change applied to Finance for Development filling the dots of the related narrative and connecting them with his extensive field experience and expertise. He defines the Theory of Change applied to the Finance for Development a process of a continuing negotiations among the Development Actors, who have different interests/aspirations/objectives/expectations in pursuing a development goal, which is dominant in the economic development’s theories. Among other, he concluded that there is nothing to change in the rules of the finance game, but the approach to deal with investment financing. Besides, Dr A. Graziosi worked out a Methodological Approach inspired by the UN 2030 Agenda along with Practical Actions to minimise the dominant role of the finance in the economy and get Capitalists involved in the real economy, referring to World Bank Group’s development schemes.

MODEL COMMUNITIES-BASED ECONOMY: What does it mean?

- To re-design the entire architecture of the approach in favour of poor people and small business as well and shift the paradigm of the financial interventions from the over-indebted economy at a micro and macro level to a real people’s empowerment through jobs creation and opportunities’ promotion.

- To have private investors really involved in the development process either directly including the Development Agencies’ Board Room or setting up a National Development Fund. (see below Options).

- To use the financial leverage for sustainable interventions, which is as much easy to say as much complicated to achieve, because it asks for a revision of the decision-making process and fulfil the credit eligibility criteria.

- To digitalise the services with a sustainable and market transparent product: this can be reached via an appropriate market segmentation [1].

- To conjugate together three main Goals of the UN 2030 Agenda for SDGs, namely Goal 1 (End of poverty), Goal 8 (Promote inclusive and sustainable growth) and Goal 17 (Partnership).

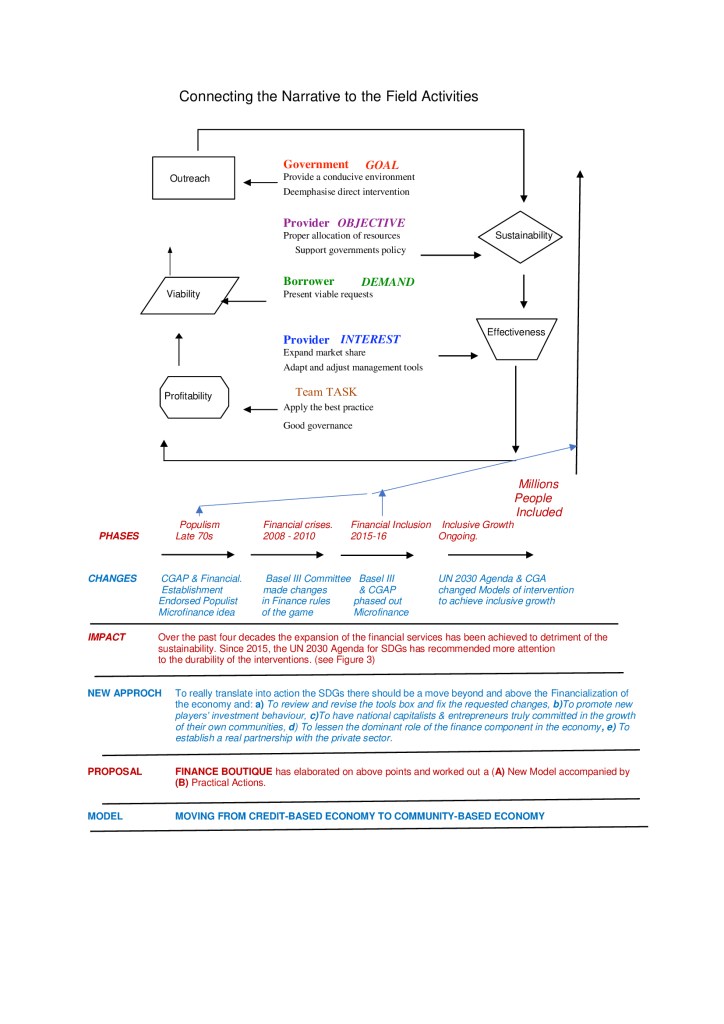

POVERTY – An Alternative Paradigm: MOVING FROM CREDIT-BASED ECONOMY to COMMUNITY BASED ECONOMY https://www.morebooks.de/store/gb/book/poverty-an-alternative-paradigm/isbn/978-613-8-45817-3

Dr Ascanio Graziosi designed a New Paradigm to tackle poverty, taking inspiration from the recent documents released by international financial establishment and borrowing from his extensive field experience and expertise on development finance issues.

The Author said that the algorithm at the heart of the capitalism, explicitly the exploitation of the natural and human resources is no more accepted either by ordinary people who are dissatisfied by the environment, or professionals and entrepreneurs involved and committed in the system.

He argued that the degeneration of the economy’s financial component hasn’t produced a real wealth, but virtual affluence. Nowadays, the accumulation has been replaced by the solidarity; however, the supporters of the solidarity idea haven’t yet proposed a new algorithm.

Day by day, people perceived that there has been something wrong in the system and in presence of above background there is a need to have a new approach to deal with inclusive growth. In this understanding the Author, referring to the UN 2030 Agenda SDGs worked out a a Model to move from CREDIT-BASED ECONOMY to COMMUNITY-BASED ECONOMY, to improve people life and business prosperity. On the matter he made a practical example referring to $ billion 2.0 IFC Programme for MENA Countries.

THE GATEWAY TO AFRICA INCLUSIVE GROWTH https://www.morebooks.de/store/gb/book/the-gateway-to-africa-inclusive-growth-jambo-fund/isbn/978-620-2-28375-5

Gateway to Africa Inclusive Growth decidedly isn’t another title to add to the overwhelming narrative on the subject, which the Author has reviewed. Then, Dr Graziosi complemented the desk research with an extensive field experience in the Continent along with the profound expertise in development finance issues, in particular Credit Guarantee Fund/ Trust Fund/ Grant Facility/ Revolving Fund, which designed, managed and evaluated in fourteen Countries. He conceived JAMBO FUND in the picture of the Community-based economy as a new approach replacing Credit-based economy. JAMBO isn’t a fund as usual; it is a Risk Fund with a vision taken from the Objectives 1 and 8 of SDGs 2030 Agenda, which has been the reference in point to promote growth via business approach and in so doing face poverty with jobs creation. Although the FUND’s horizon is the Continent, it doesn’t mean to cover 54 Countries, although opportunities could be available everywhere. Moreover, the Model is viable for a specific request at both regional and country level world-wide.

FINANCIAL INCLUSION, Give people a job not a loan, https://itunes.apple.com/us/book/id1116912686

Dr. A. Graziosi has carried out an unusual analysis on the current financial inclusion approach and achieved innovative conclusions, combining both deskwork and lessons learned while managing and evaluating development projects over the past three decades.

The Author has developed his ideas drawing on the recommendations emerging from G-20, 2015-Post Evaluation Analysis, Rio+20 meetings and the recent launch of Sustainable Development Goals. Within this background information he has worked out a proposal within the picture of a comprehensive, genuine and structured framework, having as a reference the Consultative Document on microfinance activities released within Basel III in 2010 and then updated in 2015, all of which has inspired his work.

According to the Author, to understand the current approach to financial inclusion a preliminary step is to look into the microfinance trend, which is the main vehicle to expand financial products in favour of poor people.

He claims that, over the years, microfinance activities have disclosed situations that have been in contradiction with the fundamentals of fair contractual terms, along with inappropriate assumptions and inconsistency of the methodological approach.

Starting from this point, the Author has elaborated on Basel III document to restore a correct decision making process and, in so doing, reinstate the truthful significance of credit, which means confidence. He said that sustainable microfinance is the best way to create durable jobs and eradicate poverty.

On financial inclusion he has a pioneering position and has raised a word of caution on what he has called the easy way to digitalization of micro financial services; what is more, he claims that financial inclusion without economic inclusion could be a disillusion for the lender, an illusion for the client and a likely implosion for the community.

In this context, Dr. Graziosi provides an attractive approach, which is well synthesized in the book sub-title “Give people a job not a loan”. With this declaration the Author has almost phased out the financial way to development and replaced it with the EMPLOYMENT-BASED WAY TO DEVELOPMENT, thus re-designing the entire architecture of the approach in favour of poor people.

In addition, he has completed his viewpoint by investigating the contractual conditions of experts, consultants and practitioners working overseas with donor-funded programmes. On this matter, he has concluded that Practitioners/ Experts/Developers employment status has implications for the quality of the outcome.

Abstract: The digitalization of the financial services has disclosed risks and opportunities, the former represented by a war between the two providers, which may drive to unsustainable offers and likely financial implosions and the latter the achievement of a real financial inclusion for those we haven’t yet been included in the financial circuits. Summing up, digital providers may benefit a lot cooperating with financial providers, when it comes to design a model, which asks for expertise and experience on financial services above the ground.

Others:

Colloque sur l’inclusion financière

https://www.linkedin.com/pulse/colloque-sur-linclusion-financiere-ascanio-graziosi?trk=prof-post

Financial inclusion is a marketing matter

Marketing means a strategy, which should be part of a corporate strategy https://www.linkedin.com/pulse/financial-inclusion-marketing-matter-ascanio-graziosi?trk=mp-reader-card

Legends and Myths

Financial inclusion will be analysed with facts and figures without folklore. https://www.linkedin.com/pulse/financial-inclusion-legends-myths-ascanio-graziosi?trk=prof-post

Desires, Opportunities, Risks and Field Reality

Good intentions are one thing; implementation is another. https://www.linkedin.com/pulse/financial-inclusion-desires-opportunities-risks-field-graziosi?trk=prof-post

Re-thinking the approach to financial inclusion

There could be the risks to repeat the past mistakes because there are evidences that microfinance brand has been re-named and now is called financial inclusion. https://www.linkedin.com/pulse/re-thinking-approach-financial-inclusion-ascanio-graziosi?trk=prof-post

Financial & Economic Inclusion

The real matter to discuss is the absence of a paradigm, the promotors simple neglected to provide the Practitioners with a model.https://www.linkedin.com/groups/4682884/4682884-6082218128350212098?trk=hb_ntf_LIKED_GROUP_DISC USSION_YOU_CREATED

Financial inclusion today

Tactic without a strategy https://www.linkedin.com/pulse/financial-inclusion-today-tactic-without-strategy-ascanio-graziosi?trk=mp-reader- card

Which financial inclusion?

https://www.linkedin.com/pulse/which-financial-inclusion-ascanio-graziosi?trk=mp-reader-card

Microfinance Practitioner Profile

https://www.linkedin.com/pulse/micro-finance-practitioner-profile-ascanio-graziosi?trk=mp-reader-card

Financial inclusion – Kenya Case

https://www.linkedin.com/pulse/financial-inclusion-kenya-case-ascanio-graziosi?trk=mp-reader-card

Financial inclusion

Matching up tradition, innovation and organization https://www.linkedin.com/pulse/financial-inclusion-matching-up-tradition-innovation-ascanio-graziosi?trk=mp-reader-card

A propos de l’inclusion financière

https://www.linkedin.com/pulse/propos-de-linclusion-financiere-ascanio-graziosi?trk=mp-reader-card

Suggestions for designing new credit models, Microfinance Gateway, 06/2011 (Rated among the first five most read documents of the year) http://www.microfinancegateway.org/p/site/m/template.rc/1.9.51017/

See also my Blog (News Page)