Sharing EXPERIENCE and EXPERTISE in Development Finance issues

Our FINANCE BOUTIQUE provides Policy Decision-Makers and Private Clients with advisory services to deliver an enabling financial environment and facilitate either start-up or growth-up businesses, empowering people being the avenue to alleviate poverty.

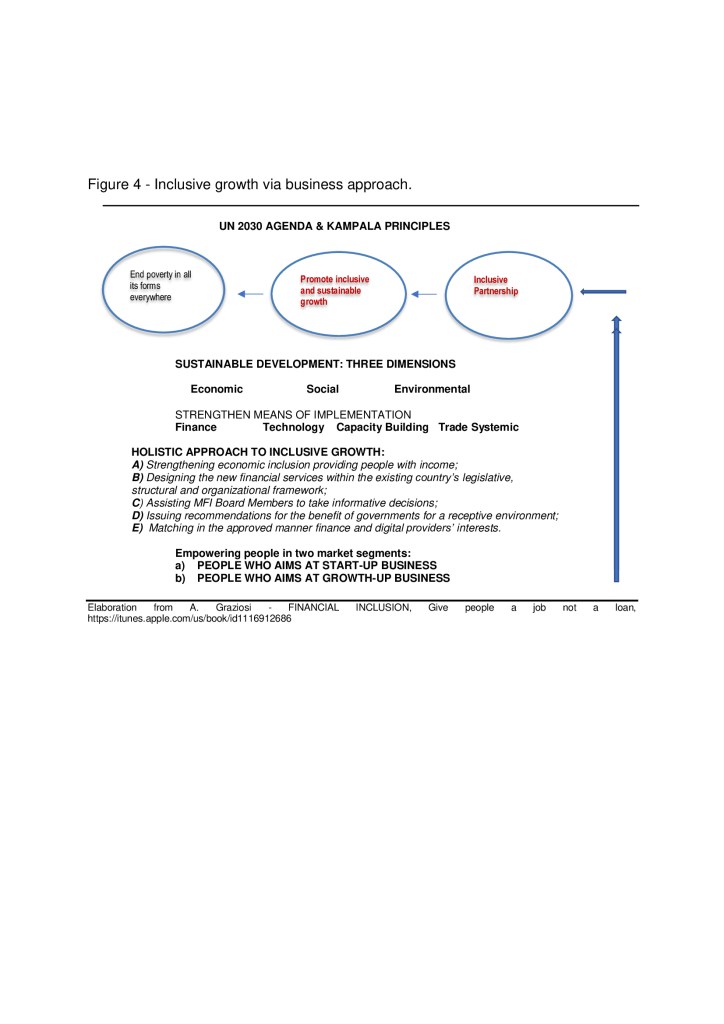

We do mix both field Experience in twenty-four Countries and Expertise in development finance to design, manage and evaluate viable and feasible business solutions to achieve countries’ inclusive growth as per the UN 2030 AGENDA FOR SDGs.

We make available services in the areas of Financial Inclusion// Retail Banking// Project Design & Management & Evaluation// Risk Fund// Revolving Fund// Governance// Microfinance// Training// Negotiation with digital & finance providers// Exploration market opportunity// Draft technical proposal & methodology for tender.

VISION – OBJECTIVES – MEANS

We have filled the dots of the financial narrative and connected them with our field experience along with the market outcome. We have assumed the Theory of Change applied to Finance for Development as a process of continuing negotiations among the Development Actors, who have different interests/aspirations/objectives/expectations in pursuing a development goal, which is dominant in the economic development theories. THE THEORY OF CHANGE APPLIED TO FINANCE FOR DEVELOPMENT http://reader.ilmiolibro.kataweb.it/v/1252660/the-theory-of-change-applied-to-finance-for-development_1268103

MOVING FROM CREDIT-BASED ECONOMY TO COMMUNITY-BASED ECONOMY. Community-Based Economy does mean to provide people with either a job or opportunities. This can’t be achieved using financial leverage alone but by conjugating together both economic policy and financial & economic inclusion, countries’ inclusive growth being the ultimate goal of the 2030 Agenda for SDGs along with lessening the finance’s dominant role in the economy and prioritizing the private sector of the economy:

- To re-design the entire architecture of the approach in favour of poor people and small business as well and shift the paradigm of the financial interventions from the over-indebted economy at a micro and macro level to a real people’s empowerment through jobs creation and opportunities’ promotion.

- To have private investors really involved in the development process either directly joying the Development Agencies’ Board Room or setting up a National Development Fund. (see below Options).

- Using financial leverage for sustainable interventions is as much easy to say as complicated to achieve because it asks for a revision of the decision-making process and fulfil the credit eligibility criteria.

- To digitalise the services with a sustainable and market-transparent product: this can be reached via appropriate market segmentation.

- To conjugate together three main Goals of the UN 2030 Agenda for SDGs, namely Goal 1 (End of poverty), Goal 8 (Promote inclusive and sustainable growth), and Goal 17 (Partnership).

The market segmentation is the core of the business of inclusive Growth when it comes to approaching the market, which deserves a correct and detailed investigation of the landscape, to understand which kind of service may be added to the product.

It also asks for making a difference among lenders, developers, and philanthropists, who have different sources of capital and use different management tools as well. In this perception, to make it a successful approach, the Stakeholders’ business behaviour will play a very important role along with the experience and expertise of the Team in charge to run the field operations.

Under the circumstances and referring to the millions of people the providers (both finance and digital) aim at having in their portfolio, we may distinguish four big market segments.

In the first segment, the financial provider is in the presence of food aid while in the second one we have income generating activities; in the third and fourth segment, the finance provider deals with promotion & enterprise development. In the Basel III’s terminology we may say that the point (a) and (b), (c) and (d) refer, respectively, to unserved and underserved customers.

It can be argued: what about the Unserved, namely the Poor who haven’t an account and couldn’t be eligible? The answer can be provided by what the African banker & tycoon Mr Elumelu said in an interview (2014) “There are some areas — flood disasters, for instance — where you must give charity. “But I think the charity approach to solving other issues must be reassessed. It’s all about sustainability; it’s all about self-reliance. It is catalytic philanthropy”. https://www.devex.com/news/tony-elumelu-s-new-africapitalism-82590

On theme of digitalisation of the financial services and the related cost for the users, we made the following Concrete Proposal : we don’t say that money transfers and remittances should be free of charge; we do say that the service should be sustainable for the provider, accessible for the potential client and affordable for the user. Technologists and Financiers should find out the way to not overcharge the transfer of small amount of money presumably made by people working away from their own places and sending money to those who are in need. If we don’t find out modalities to minimize the commission, we will penalize the poor and mislead the purpose of financial inclusion. This is a technical matter that may be overcome elaborating on the statistical data; it may be assumed, for example, a cheap commission for small amount or linking it to the frequency of the transactions in a given period. Also, it could be studied that the GVTs of poor countries may take the charge of the commission or part of it.